The US healthcare industry has never been a simple industry to run. But right now, the complexity feels different, less like the normal friction of a massive system and more like a slow recalibration that nobody fully controls. Costs are rising faster than reimbursements. Labor shortages haven't been fully resolved. Policymakers are rewriting the rules on Medicaid, ACA subsidies, and drug pricing mid-game. And somewhere in the middle of all this pressure, artificial intelligence is being asked to save the day.

What's striking about the current moment isn't any single trend in isolation, it's how they're converging at the same time.

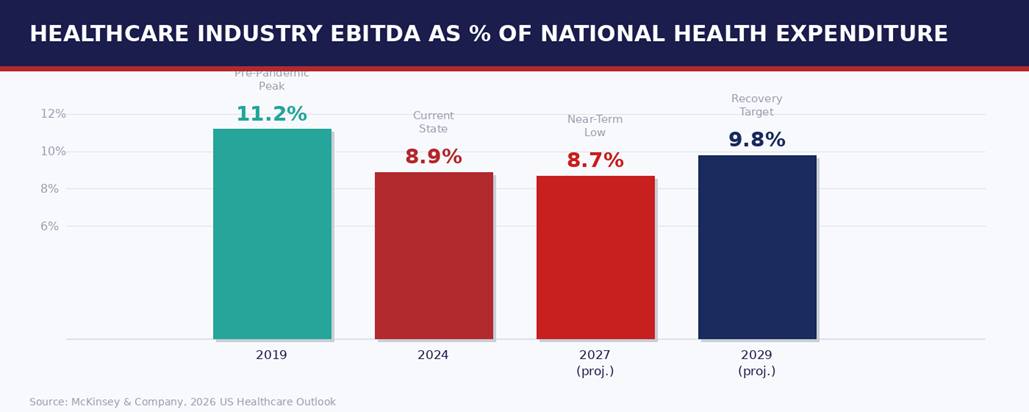

Let's start with the financial reality, because everything else flows from it. Healthcare's overall profitability, measured as industry EBITDA against national health expenditure, has been eroding for years.

Payers and providers have absorbed the most pressure. Payers in particular had a brutal 2024: overall EBITDA for the sector dropped from roughly $61 billion in 2023 to approximately $29 billion the following year, driven by a combination of higher utilization, regulatory disruption, and the ripple effects of pandemic-era enrollment shifts unwinding. Providers saw modest margin recovery, from 8.9% in 2023 to 9.1% in 2024, but remain below pre-pandemic performance.

"Healthcare organizations generating less return per dollar of national spending than six years ago; that trend is continuing, and strategy must account for it."

The path forward looks different depending on which segment you're in. For payers and providers, 2024 through 2027 will be a period of grinding through, managing costs, repricing products, and finding efficiencies where they can. The stronger growth window is expected to open after 2027 as enrollment shifts stabilize and employers absorb workers currently losing Medicaid coverage.

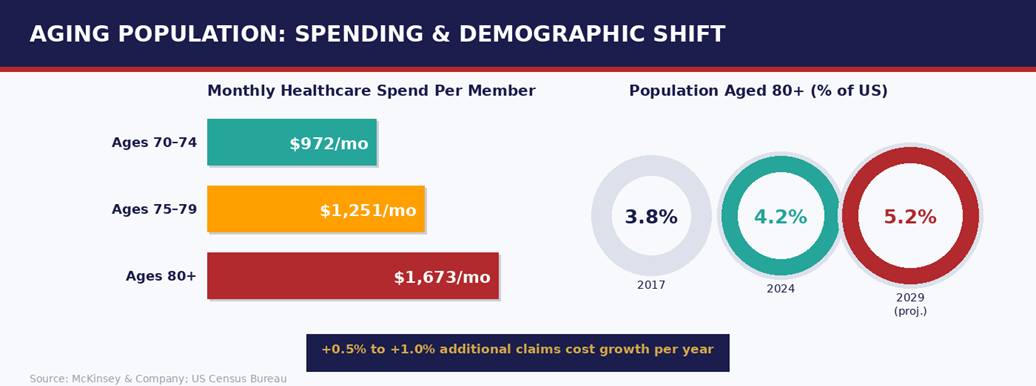

Understanding where the financial pressure comes from matters more than simply acknowledging it exists. Two forces above all others are driving claims cost inflation: the aging of the population and the explosion of pharmaceutical spending.

The share of Americans aged 80 and older grew from 3.8% in 2017 to 4.2% in 2024, and is expected to reach 5.2% by 2029, according to the US Census Bureau data. That may sound like a modest shift, but the cost implications are steep. Monthly healthcare spending for someone aged 70 to 74 averages around $972. For those between 75 and 79, it's $1,251. For individuals 80 and above, it reaches $1,673.

McKinsey estimates this demographic trajectory alone will add 0.5% to 1.0% to claims costs annually, a sustained, compounding drag on payer financials. Neither of these forces is going away. They're structural, not cyclical, and any strategy built on waiting them out will fail.

The payer sector is not one market; it's four or five markets moving in very different directions simultaneously. Group commercial insurance is emerging as the clearest bright spot. As Medicaid disenrollments accelerate, potentially affecting nine million to ten million individuals by 2027 under current policy trajectories, a meaningful subset of them are already working and could transition to employer-sponsored coverage.

Medicare Advantage is in recovery mode. Margins were essentially at breakeven in 2024, with about 72% of plans operating in negative EBITDA territory. A gradual improvement is expected from 2026 onward, with margins normalizing around 2% by 2029. Medicaid is the most challenged segment in the near term, the expiration of pandemic-era policy protections triggered significant enrollment loss and adverse risk selection, potentially pushing Medicaid EBITDA into negative territory before a slow recovery begins in 2029.

The provider story in 2026 is really a story about geography within the care continuum, specifically, about which settings are gaining volume and which are losing it. The direction is unmistakable: care is moving away from hospital inpatient settings toward lower-cost, higher-flexibility outpatient and home-based environments.

General acute hospitals are managing a narrow path. Margins are expected to grow from 6.8% in 2024 to 7.6% by 2029, but the recovery will be uneven, compressed in the 2025 to 2027 window by tariff-driven supply cost increases, subsidy expirations, and potential site neutrality policies. Hospitals' share of overall provider profits is expected to decline from 41% in 2019 to around 38% by 2029 as care migrates elsewhere.

"Post-acute care is positioned for stronger performance over the next several years, hospice projected at 9% annual growth, home health at 6%, as demographic aging and Medicare expansion accelerate demand."

Skilled nursing facilities face a harder path: shorter stays, payer-directed discharge patterns, and ongoing labor and compliance cost pressure are limiting margin improvement. Office-based specialty care is holding up better than primary care, supported by growing demand for ancillary services like diagnostics and imaging.

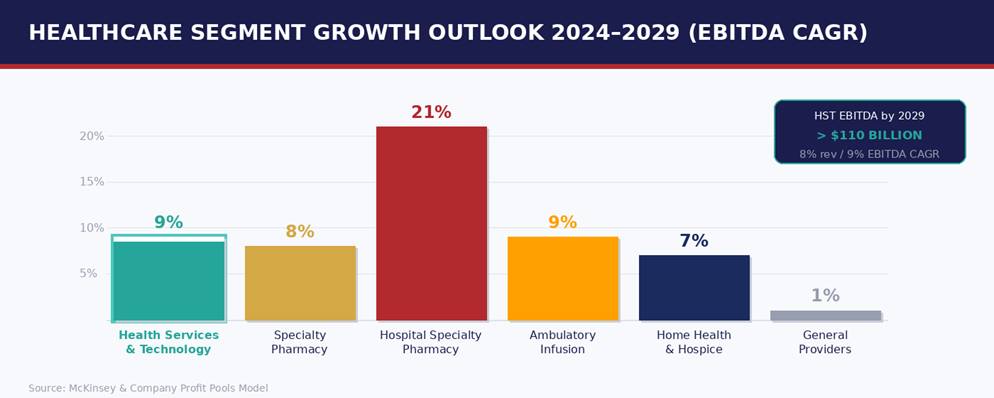

While payers and providers navigate a difficult few years, one segment of healthcare is growing rapidly and consistently: Health Services and Technology. HST is projected to be the fastest-growing sector in healthcare through 2029, 8% annual revenue growth and 9% annual EBITDA growth, with total HST EBITDA expected to surpass $110 billion by 2029.

The underlying dynamic is straightforward: payers and providers under financial pressure are outsourcing more administrative and operational functions to technology platforms. Revenue cycle management, claims processing, prior authorization, clinical documentation, all of these are becoming increasingly tech-enabled, and the value is accruing to the platforms that handle them well.

Within HST, software and data analytics are the fastest-growing subsegments. The top 25 HST companies already represent about 29% of total HST revenue, up from 20% in 2019. Venture capital deployment into HST exceeded $11 billion in both 2023 and 2024, reaching $11.9 billion in just the first three quarters of 2025 alone.

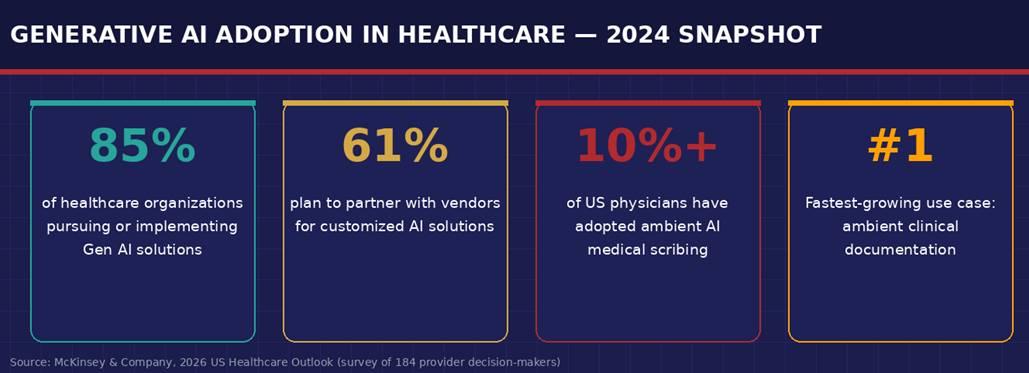

The conversation about AI in healthcare used to center on potential. That conversation has shifted. As of 2024, 85% of healthcare organizations surveyed by McKinsey were actively pursuing or had already implemented generative AI solutions. Among those organizations, 61% planned to work with external vendors to develop solutions tailored to their specific workflows.

The clearest current example of at-scale adoption is ambient clinical documentation. AI tools that listen to physician-patient conversations and automatically generate clinical notes have moved from early pilots to meaningful penetration: McKinsey estimates that 10% or more of US physicians have now adopted some form of ambient scribing. For a technology that barely existed outside venture-backed startups five years ago, that is a significant deployment curve.

"AI is gaining adoption fastest in places where the return on investment is measurable and near-term. Healthcare organizations under margin pressure aren't funding moonshots, they're funding tools that demonstrably reduce administrative cost."

The more transformative applications are in revenue cycle management and administrative workflows. AI-enabled claims processing, predictive denial management, and automated prior authorization are all moving from experimentation toward implementation. The financial case is direct: lower cost-to-collect, fewer denied claims, faster reimbursement cycles.

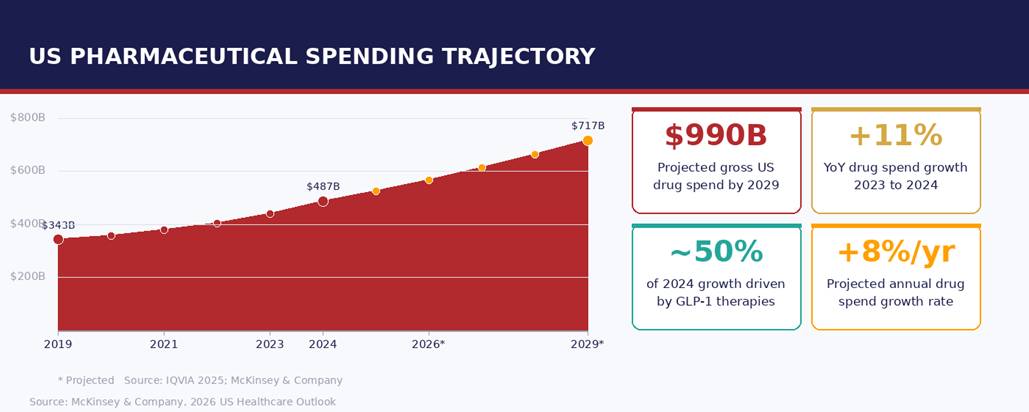

Specialty pharmacy and infusion services are among the most significant growth vectors in healthcare right now, and also among the most operationally demanding. Drug spending growth at 11% year-over-year in 2024 is not a number that happens in steady-state markets. It reflects the rapid mainstreaming of biologic therapies, GLP-1 agonists, and high-cost specialty injectables across a broader patient population.

Hospital specialty pharmacy services alone are projected to grow at 21% annually through 2029, with ambulatory infusion not far behind at 9% annually. Managing that growth requires infrastructure that most practices weren't originally built for. Prior authorization workflows, infusion scheduling, specialty drug inventory, reimbursement tracking, and documentation requirements all compound on each other in ways that overwhelm manual processes quickly.

Practices and health systems expanding into this space are finding that the operational complexity scales faster than the revenue does, at least without the right systems in place. Connected workflows that can handle the full cycle from order to reimbursement, without requiring constant manual intervention, are no longer nice-to-have. For practices building serious infusion programs or expanding specialty pharmacy capabilities, they're a prerequisite for margin sustainability.

The healthcare organizations that navigate this period well won't do so by waiting for macro conditions to improve. The improvement that McKinsey projects after 2027, stronger EBITDA growth, recovering payer margins, enrollment stabilization, is contingent on organizations taking specific actions in the near term to build the operational foundation for it.

Those actions are consistent across segments: reducing administrative overhead through automation, investing in revenue cycle capabilities that protect reimbursement, building or acquiring technology platforms that can scale with volume, and making deliberate decisions about which care settings and service lines to prioritize as the site-of-care shift accelerates.

"The organizations building scalable infrastructure now, in technology, in workflows, in revenue cycle management, are positioning themselves for a recovery that will create real competitive distance from those that didn't."

The healthcare system is not broken. But it is under sustained financial and demographic pressure that will reward operational discipline and punish inertia. The reckoning that 2026 represents isn't an ending. It's a reordering. The question is which side of that reordering your organization is on.

Sources:

You may like these too…